THE WHEY FORWARD 2026/27

Five forces are now reshaping the economics of dairy, and the window to act is narrower than most boardrooms appreciate

Executive Summary

When we last wrote on whey in The Dairy Mail, the argument was that the byproduct was quietly being repositioned as a strategic asset. Six months on, that repositioning is neither quiet nor gradual. Whey has inverted. At the close of Q1 2026, European whey protein isolate is trading near record highs around £20,200 per tonne, US WPI has cleared £8/lb, and major processors have sold forward WPC80 and WPI contracts well into late 2026. Prime commodity dairy, butter in particular, remains under surplus pressure. Cheese plants in the United States are now reporting that whey is generating more margin than the cheese itself. That reversal has no obvious precedent.

This briefing sets out the five forces now reshaping the whey and protein economy for 2026 and 2027. The first is a processing-capacity shortage that will not ease before late 2027. The second is the consumer realignment GLP-1 adoption has already triggered in grocery. The third is the mainstreaming of clear-whey formats. The fourth is the widening British processing gap. The fifth is whey’s move into pharma-adjacent applications, from medical nutrition to cosmeceuticals. UK and Irish producers have a window. It will close by 2028 once North American and continental capacity additions rebalance supply. Firms that commit capex now will capture premium margin for a decade. Those who continue to ship unrefined whey across the Irish Sea will watch the value accrue elsewhere.

FORCE 1

The Structural Inversion

Whey is no longer behaving like a dairy commodity. Through 2023 and into 2024, high-quality whey protein traded below £3/lb. By late 2025 the benchmark had broken above £8/lb, with some US WPI contracts clearing £9. Vesper’s end-January 2026 read put European WPI instant at £20,200/tonne, with WPC80 at £12,460/tonne. Producers are not just raising prices; they have sold out of inventory and in several categories moved to a made-to-order posture. Read that as supplier power, not as the usual pricing cycle.

The cause is not a milk shortage. Global dairy supply is comfortable. Rabobank expects the ‘big seven’ dairy exporters to grow output by around 0.2% in 2026, a slowdown on the 2.6% expansion of the prior year but still substantial tonnage at farmgate. The bottleneck sits one step downstream, in the specialist fractionation plants. Ultrafiltration and spray-drying capacity cannot be built quickly. US WPC production was up nearly 19% year-on-year in November 2025 and still could not meet demand. The mismatch between plentiful commodity processing and scarce specialist fractionation will persist until the wave of announced capacity starts depositing meaningful volume in late 2026 and 2027.

“Almost weekly, you hear about an investment increasing capacity for high proteins.”

John Lancaster, Head of EMEA Dairy & Food Consulting, StoneX

For an MD, the practical implication is straightforward. Whey now needs to sit as a line on the P&L with its own strategy and its own capex case. The cheesemaker who still treats whey revenue as something that mainly covers disposal costs is planning for the market of 2019, not 2026.

FORCE 2

GLP-1: Permanent Consumption Realignment

GLP-1 is the consumer-demand driver that broke this market, and every signal says it is still deepening. GLP-1 receptor agonists, the class containing semaglutide and tirzepatide, have moved from clinical niche to mass adoption faster than any drug category in recent memory. Gallup’s October 2025 data put US adult usage of injectable GLP-1s for weight loss at 12.4%. AHDB’s February 2026 analysis noted UK household penetration at around 4.1%, with European uptake still in its early innings. The Cornell-Numerator panel study, published in the Journal of Marketing Research in January 2026, found GLP-1 households reduced total grocery spend by about 6% within six months of adoption. The reduction landed hardest on ultra-processed snacks and sweets; high-protein categories gained share.

The important point is that GLP-1 has reshaped protein demand rather than shrunk it. The pie is modestly smaller, but the high-protein slice is materially larger. In UK grocery, NielsenIQ’s 4-week read to late January 2026 put protein-claim food sales up 9.6% and fibre-claim up 14.1%, both comfortably ahead of total FMCG. Kantar’s 52-week read to 28 December 2025 put UK cottage cheese sales up 41.9% in value to £102.2m, with volume up 28.1%. Kefir and Greek yogurt are in double-digit growth. Whey-fortified desserts and high-protein cheddar are on shelf in volumes that would have been speculative three years ago. The dairy fixture is being re-ranged around protein density.

The question every processor should be asking has moved on from whether GLP-1 is a fad. The real question is whether their product portfolio looks right for a world in which, by 2028, an estimated one in four US adults and perhaps one in ten UK adults will be managing appetite pharmacologically. Semaglutide patent expiries in China, India, Brazil and Turkey land through 2026. The adoption curve ahead is steeper than the one behind us.

“Dairy is well placed to benefit from the ‘less but better’ trend.”

RaboResearch, cited in AHDB GLP-1 market analysis (February 2026)

FORCE 3

Format Disruption: Clear Whey Mainstreams

Format is the force most commercially actionable for an innovation director. Clear whey, the shift from milky protein shakes to transparent juice-style drinks, has moved past the early-adopter phase. Research & Markets data valued the global clear whey isolate category at around £338m in 2024. Estimates put 2026 near £5bn once lifestyle and functional beverage extensions are included. European NPD in the category grew more than 50% net over the twelve months to mid-2025 (Nutrition Integrated).

The opportunity structure is unusual. In the UK and EU, only about one in five whey brands currently offers a clear-whey variant. That leaves real white space, and it is being taken by the firms moving fastest. Tirlán’s £110m commitment to its Ballyragget site, announced in November 2025 and due on-stream by mid-2027, is oriented explicitly to clear whey protein isolate for lifestyle and performance nutrition. FrieslandCampina has acquired Wisconsin Whey Protein. Fonterra, Glanbia and Arla Foods Ingredients between them now control more than 45% of global isolate capacity, according to Mordor Intelligence’s January 2026 market note.

“This project isn’t just about building capacity; it’s a platform for long-term growth.”

John Murphy, Chairperson, Tirlán (on the £110m Ballyragget investment)

Format innovation matters because it reopens price elasticity. A clear whey beverage sells into hydration, sports and lifestyle occasions where a traditional milky shake does not, and commands roughly 20–30% higher margin per gram of protein. For British and Irish processors with the raw milk quality story already in place, the clear-whey category is the most defensible near-term margin play available. It is also where UK own-label is moving at pace. M&S, Co-op, Morrisons and Waitrose are all building private-label ranges around GLP-1-aligned high-protein formats.

FORCE 4

The UK Processing Gap

This is the uncomfortable part of the argument. AHDB’s 2025 trade review, published in February 2026, reported UK whey and whey product exports up 10,100 tonnes (+16.6%) year-on-year, adding £24m in value. That is the second consecutive year of growth, explicitly linked to GLP-1 and dairy protein demand. Cheese exports hit £971m, up 9.4%. Butter up 14.3%. On the surface, the UK dairy export performance is strong. Look one layer down and the picture is more ambivalent.

Much of the UK’s whey export volume is WPC35 or unrefined sweet whey powder, priced in a narrow band close to £1,000/tonne. The value-added product, the WPC80, WPI, hydrolysates and specialty fractions where the margin sits, is mostly processed on the continent. Ireland, the Netherlands, Germany and Denmark take the bulk of it. AHDB’s own analysis puts it plainly: cheese is readily processed in GB, but enhanced whey products are more readily processed on the continent. That sentence, dropped into a late-February market note, deserves a full board-level discussion. It is the single most important competitive disadvantage British dairy carries into 2026.

The evidence of continental ambition is not subtle. Ireland’s Tirlán has committed £110m. FrieslandCampina is expanding its Wisconsin Whey WPI plant to 10,000 tonnes annual capacity. Idaho Milk Products has invested approximately £148m in blending infrastructure. Fonterra has committed around £50m to its Studholme protein hub. Glanbia is adding roughly 4,500 tonnes of WPI capacity through its Southwest Cheese joint venture. The UK’s equivalent pipeline, measured in dedicated specialty whey capacity rather than general processing, does not yet compare. The Arla and First Milk WPC co-manufacturing arrangement, announced in 2022, remains the most substantive UK-focused move of recent years.

“These trends justify the expanded processing capacity now being built.”

Lucas Fuess, Senior Dairy Analyst, RaboResearch

British demand for whey is clear and accelerating. The open question is whether UK processors capture the margin that demand will produce, or continue to export the raw material and import the refined product. If current trajectories hold, the UK will by 2028 run a structural deficit in specialty whey proteins while running a growing surplus in cheese and raw whey. That is the trade pattern of value leaving the country.

FORCE 5

The Bioeconomy Frontier

This is where the forward-looking capital will flow over the 2026–28 horizon: beyond sports nutrition into medical, infant and cosmeceutical applications. Whey’s leucine content and rapid absorption make it the clinically preferred protein for muscle preservation in GLP-1 therapy and for sarcopenia management in ageing populations. It is equally relevant in critical-care nutrition. Mordor Intelligence flags Asia-Pacific infant formula and halal-compliant sourcing as the fastest-growing regional demand drivers. Arla Foods Ingredients has a new hydrolysate range aimed specifically at easier-digesting infant nutrition. Tirlán’s own stated targets include infant formula and medical nutrition alongside lifestyle.

Cosmetic and cosmeceutical applications remain smaller in absolute revenue. Whey-derived bioactive peptides, lactose-based humectants and lactic-acid fractions are niche volumes today, but they carry disproportionate brand and sustainability equity. They fit the closed-loop narrative that regulators and retailers increasingly demand, and they fit the CSRD and DMCCA reporting environment that will govern 2026–28 sustainability disclosures across British and Irish businesses supplying EU customers. A WPI sold into a skincare line traceable to a named Irish grass-fed herd is worth more per kilogram than the same WPI sold into a commodity supplement. The premium is not marginal.

The practical point for British and Irish producers is that the bioeconomy frontier is where the protein-shortage argument meets the sustainability-reporting argument. Buyers are beginning to ask for a single integrated proposition: a high-purity fraction with verifiable grass-fed origin and an auditable Scope 3 position. A firm that can deliver all three has written the spec sheet buyers will be using in 2027.

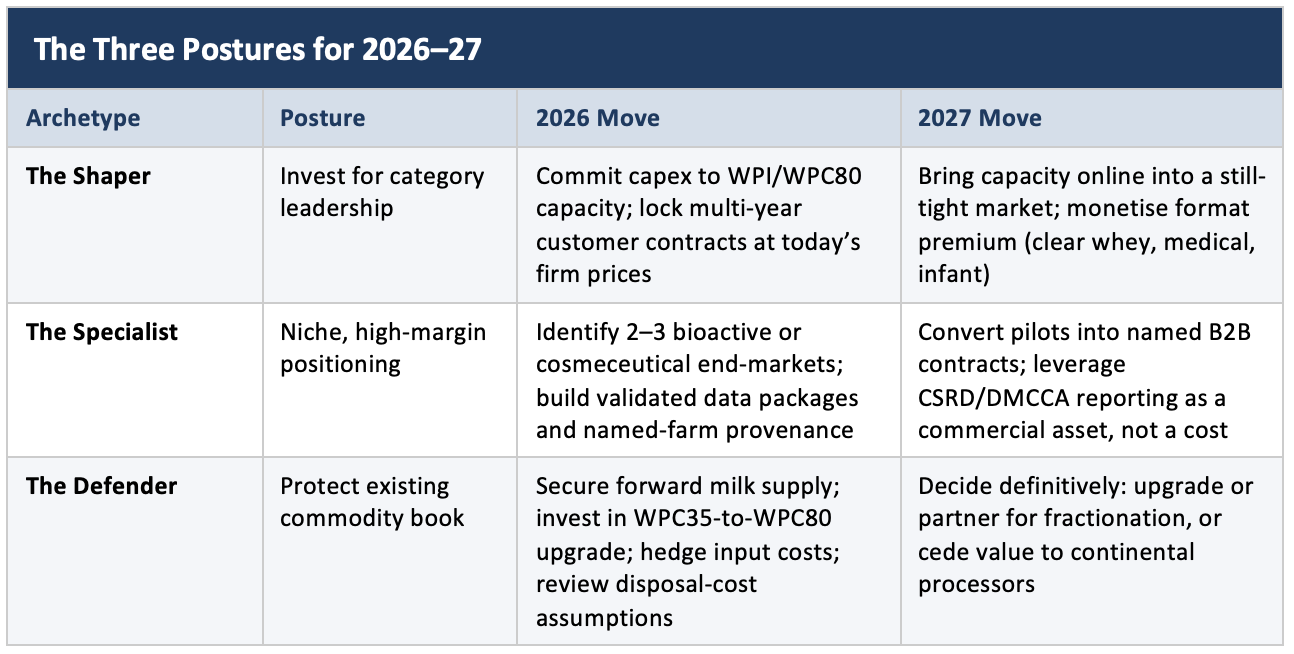

The test for each posture is the same. Does the organisation emerge from 2027 with greater pricing power per kilogram of protein sold than it had in 2024? If the honest answer is no, the strategy is not working, regardless of top-line growth.

Closing COMMENTS: The Window Closes by 2028

The temptation is to describe whey as a generational opportunity. The window is considerably shorter than that. Three years, closing hard.

By late 2027, a wave of announced capacity begins to land. Tirlán in Ballyragget, Glanbia in New Mexico, FrieslandCampina in Wisconsin, Idaho Milk Products, Fonterra in Studholme, and the broader US cheese plant build-out will between them deposit meaningful WPC80 and WPI volume into global markets. Rabobank’s cautious price recovery thesis for 2026 becomes a more ambiguous picture by 2028. Prices will remain higher than 2023 lows, but the extraordinary premium visible today will compress.

The firms that will capture value from that compression are the ones entering now, at 2026 construction costs, for capacity that lands inside the tight 2026–27 window, with customer contracts signed against today’s price environment. Firms that enter in 2028 will be paying 2028 construction costs to build 2028 capacity into a 2028 market. The return profile is nothing like the conventional dairy-commodity investment case, which has historically rewarded patience.

This is the argument UK and Irish industry needs to have out loud, and in the next two quarters rather than the next two years. The protein supply squeeze is real and it is time-limited. GLP-1 has permanently changed what the British shopper will put in their basket. Clear whey has moved beyond format trend and become the entry point to a billion-pound category. The bioeconomy frontier is where the 2030 margin will sit. The UK processing gap, uncomfortable to state plainly, is the one element on that list within domestic strategic control.

The original Whey Forward article closed with a line about conviction. Six months on, the observation still holds, but the stakes have risen. A producer who treats whey as a disposal problem in 2026 will find themselves explaining to their board in 2028 why margin accrued to Kilkenny, Wisconsin and Videbæk rather than to them. The alternative is to treat whey as the most important strategic asset on the balance sheet and behave accordingly, at pace. That choice will define the next decade of British and Irish dairy competitiveness.

The decision now in front of UK and Irish dairy boards is a capex commitment on a twenty-four month clock. There is no extension available.

Steve Moncrieff is Founder and Managing Director of the Dairy Connect Group, publisher of The Dairy Mail, and Founder and Strategy Director of the International Cheese & Dairy Awards and International Cheese & Dairy EXPO, taking place 24–25 June 2026.

Sources referenced: AHDB dairy trade review and market commentary (Feb–Mar 2026); Kantar FMCG and category data (to 28 Dec 2025); NielsenIQ UK shopper insight (Feb 2026); Mintel consumer and F&B strategic analysis (2025–26); Rabobank ‘Cautious Dairy Commodity Price Recovery’ and Global Animal Protein Outlook 2026; Mordor Intelligence whey protein market outlook (Jan 2026); Vesper Price Index whey commentary (Nov 2025, Jan 2026); Fortune Business Insights Whey Protein Market Report 2034; Ever.Ag Insight whey price tracking; Cornell University / Numerator, Journal of Marketing Research (2025). All currency figures converted to GBP at April 2026 rates.

More news and insight