THE CUSTOMER THE PROTEIN AISLE FORGOT

THE COTTAGE CHEESE BOOM LOOKS LIKE A TIKTOK STORY. THE CHECKOUT DATA TELLS A DIFFERENT ONE — AND SO DOES THE DEMOGRAPHIC CURVE BEHIND IT.

NIQ’s full-year UK protein dairy readout to 27 December 2025 complicates two prior pieces in this column. November’s white paper segmented the cottage cheese boom across its millennial and Gen Z shopper base. March’s GLP-1 column asked whether dairy was prepared to lead the protein conversation or let others define it. The till has now answered both, in a way few brand briefs anticipated. The shopper adding the largest single slice of incremental value to UK protein dairy is at least three decades older than the imagery on most packs.

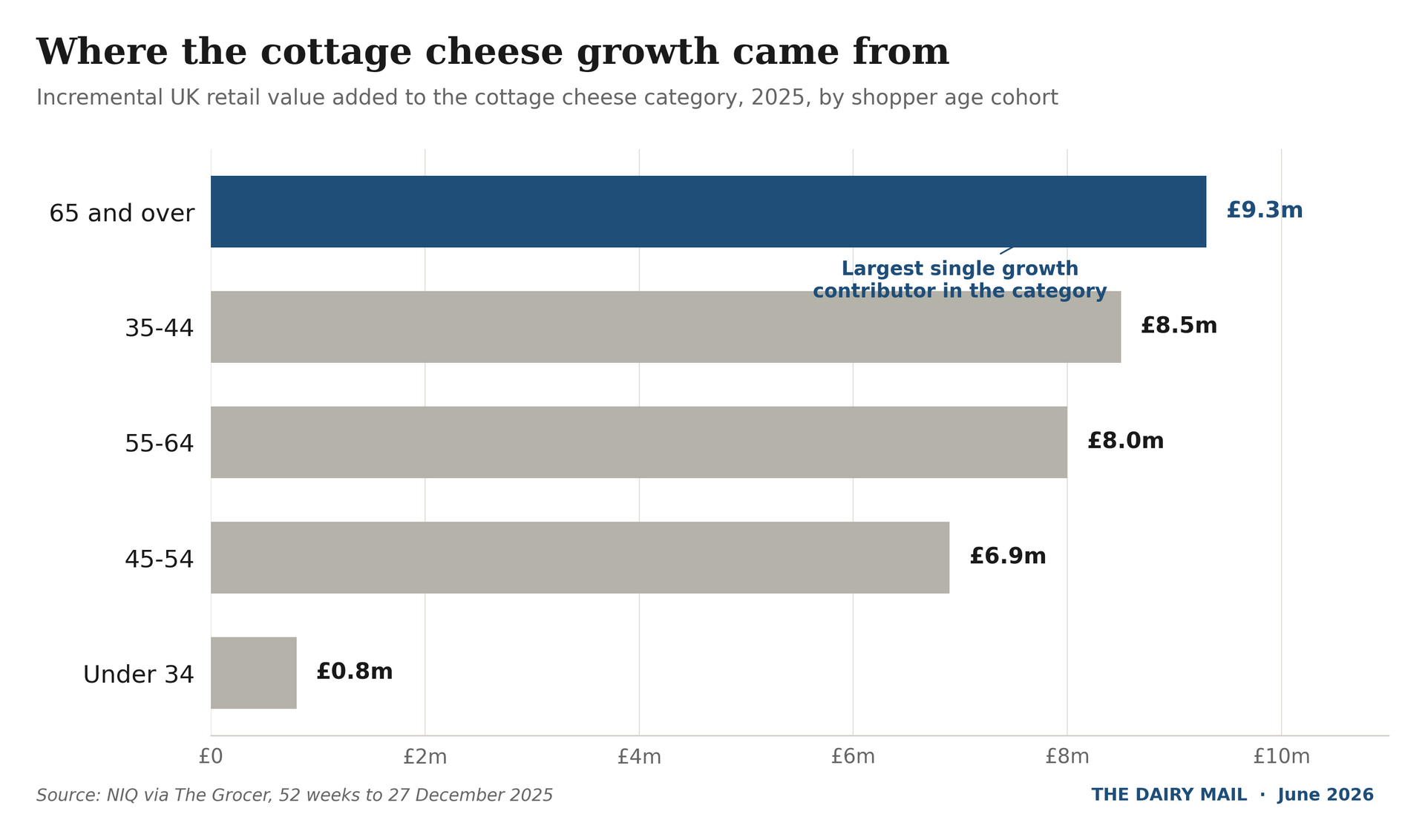

Cottage Cheese: Who Added the Value

The cottage cheese numbers carry the cleanest illustration. Of the £37.2m of incremental value the category added in twelve months, shoppers aged 65 and over contributed £9.3m of growth, taking that age cohort to £26.1m in annual spend. The under-34s, the demographic to which the cottage cheese revival has been widely credited, added £0.8m. The category grew 200% at Tesco over two years on the back of a customer the industry was barely talking to.

Beyond Cottage Cheese: Signals Across Protein Dairy

The same signal sits across protein dairy more broadly. Müller’s Myprotein co-branded range added £21.9m in 2025, almost half of the parent brand’s total uplift, while Müller Light, the diet-positioned product of a previous demographic moment, has been quietly slipping. Arla closed 2025 with Arla Protein volumes up 19.5% and Arla Skyr up 17.8%; chief executive Peder Tuborgh told reporters in February that protein demand was being driven by “demographic changes globally as well as consumer trends such as weight management”. The co-op’s acquisition of Volac’s whey processing facility in Wales has positioned protein as a balance-sheet priority rather than an innovation pilot.

The Demographic Reallocation Underneath the Numbers

The demographic reallocation underneath the protein numbers is quieter and far larger than the headline reads. The Office for National Statistics puts the UK pensionable-age population at 12.4 million, rising to 14.2 million by mid-2034, an additional 1.8 million older consumers in under a decade. The working-age population is growing far more slowly, and the birth rate has fallen to a record low of 1.49. The International Longevity Centre’s most recent analysis has the over-50s already accounting for 54% of UK consumer spending, projected to reach 63% by 2040. In a country where deaths are forecast to exceed births from this year onwards, the dairy category sits in the unusual position of having its largest absolute demographic also be its fastest-growing one.

Clinical Requirements: Older Adults and Protein

The clinical case has been catching up with the commercial one. The British Dietetic Association puts sarcopenia prevalence at between 4% and 25% of free-living older adults in the UK, a range wide enough to imply both clinical underdiagnosis and considerable preventative headroom. Dietary guidance has lagged the science. The UK Reference Nutrient Intake for protein remains 0.75g per kilogram per day, while recent indicator amino acid oxidation work published in Frontiers in Nutrition put the requirement for older adults with sarcopenia at 1.21 to 1.54g per kilogram per day. The implication for dairy is direct. Greek yoghurt, skyr, quark and cottage cheese deliver complete protein at concentrations and leucine ratios other affordable, ambient-friendly food categories cannot easily match.

GLP-1 Acceleration: Clinical Instruction, Not Marketing

GLP-1 prescribing has accelerated the same trajectory from a different direction. A University College London analysis published in BMC Medicine estimates around 1.6 million UK adults used a GLP-1 weight-loss medication in the year to early 2025; IQVIA’s dispensed-prescription data put more than two million paying privately by July, making Britain the largest anti-obesity medicines market in Europe. Most of those users are losing weight on a flattened appetite, which has turned protein density into a clinical instruction rather than a fitness marketing claim. The patient leaving the GP surgery with a Mounjaro pen is being advised to eat more cottage cheese, not less.

Behavioural and Format Shifts: From Identity to Insurance

The behavioural shift concerns the identity of the protein buyer rather than the salience of the macronutrient itself. Sports nutrition built its mid-decade growth on a customer who chose protein as identity. The customer now driving the next leg of the category buys protein as insurance, and shops with the slower cadence of household replenishment rather than gym-bag urgency. Format follows from this. The 825g and 1kg skyr tubs that Yoplait reports driving incremental UK sales look much more like a household staple than a single-portion gym SKU.

Corporate Signals: Where Capital Thinks Growth Is

The Lactalis Group’s acquisition of Protein Works on 1 June, four days before this column went to press, is the most instructive deal for reading where dairy capital currently believes protein growth lies. The Liverpool-based business turned over £55m to August 2025 and runs a direct-to-consumer model from its Speke facility, with a catalogue spanning shakes, meal replacements, wellness supplements and high-protein snacks. Where Arla spent in Wales for processing capacity, Lactalis has spent in Liverpool for brand equity. Chairman Emmanuel Besnier framed the purchase as a play on “the fast-growing active nutrition market”. The positioning the deal puts on Lactalis’s balance sheet is anchored to a sports-and-performance reading the demographic now driving category value walks past. Protein Works’ catalogue already includes GLP-1-friendly shakes, which signals where the brand will eventually need to flex; the deal communications, for now, do not.

Implications for Brands and Retailers

Several uncomfortable consequences follow for the trade. Brand imagery across protein dairy remains relentlessly youthful and post-workout in tone, while the value being added to the till comes from a demographic that does not see itself in any of it. Private label has moved faster than the brands: NIQ has retailer-own cottage cheese volumes at 16.1 million kilograms in 2025, up 35% year-on-year, against the largest branded player at roughly a fifth of that figure. Branded growth that fails to widen its visual and editorial address will continue losing share to supermarket lines that simply put the product on shelf, without an aesthetic the over-65 shopper has to mentally edit out.

The retail planogram and the brand brief have yet to catch up with the basket. The most valuable protein-dairy convert in Britain over the next ten years is a customer the category has been quietly serving for a generation, and continues, at considerable commercial cost, to photograph as someone else.

This is the third instalment in this column's reading of UK protein dairy through 2025–26, following November's white paper on cottage cheese and March's analysis of dairy's GLP-1 opportunity, both available at thedairymail.com. For continuing weekly analysis of UK dairy category and demographic shifts, subscribe to Dairy Connect Briefing.

Q&A

Who is actually driving the UK protein dairy boom?

Short answer: Older shoppers, not Gen Z or millennials. In cottage cheese—the clearest case—over-65s contributed £9.3m of the £37.2m incremental value added in the past year, taking their annual spend to £26.1m, while under-34s added just £0.8m. Tesco’s cottage cheese sales grew 200% over two years largely on the back of this older customer. Across protein dairy, Müller’s Myprotein co-branded range added £21.9m in 2025 even as Müller Light slipped, underscoring that protein growth is coming from a different buyer and need-state than the category’s youthful, post-workout imagery suggests.

Why does the UK’s demographic curve matter so much for protein dairy?

Short answer: Because the UK’s largest demographic is also its fastest-growing—and it already controls most consumer spend. The pensionable-age population stands at 12.4 million and is projected to reach 14.2 million by mid-2034 (+1.8 million), while births fall to record lows (1.49 fertility rate) and deaths are forecast to exceed births. Over-50s already account for 54% of UK consumer spending, projected to hit 63% by 2040. Protein dairy sits squarely in this demand stream.

What clinical shifts are changing protein needs for older adults—and why is dairy well placed?

Short answer: Sarcopenia affects an estimated 4%–25% of free-living older adults in the UK, and evolving science suggests many need far more protein than legacy guidance. The UK RNI remains 0.75 g/kg/day, but recent indicator amino acid oxidation research indicates older adults with sarcopenia may require 1.21–1.54 g/kg/day. Dairy formats like Greek yoghurt, skyr, quark, and cottage cheese deliver complete, leucine-rich protein at accessible prices and in convenient formats that other ambient categories struggle to match.

How are GLP-1 weight-loss medicines reshaping protein purchasing and formats?

Short answer: With 1.6 million UK adults using GLP-1s in the year to early 2025 and over two million paying privately by July, protein density has become a clinical instruction, not a gym slogan. Appetite suppression shifts baskets toward high-protein options such as cottage cheese. The buyer now shops with household-replenishment cadence, favoring larger formats—like the 825g and 1kg skyr tubs Yoplait cites as incremental drivers—over single-serve “gym” SKUs.

What should brands and retailers change now—and how do recent corporate bets stack up?

Short answer: Update the brief to match the basket. Widen brand imagery and copy to include older shoppers; prioritize household formats; and rework planograms for replenishment buying. Private label is already capitalizing—retailer-own cottage cheese hit 16.1m kg in 2025, up 35% year-on-year, versus the top brand at roughly a fifth of that volume—so brands that stay locked in youthful, post-workout aesthetics risk ceding share. Strategically, Arla’s investment in whey capacity and strong Arla Protein/Skyr growth aligns with durable demand; Müller’s Myprotein uplift shows co-branding can work. Lactalis’s Protein Works deal targets “active nutrition,” but growth is being driven by an older, insurance-minded buyer; the portfolio’s GLP-1-friendly shakes hint at where it can pivot, even if the deal communications don’t yet reflect that.

SOURCES

Retail and category data. NIQ via The Grocer, 52 weeks to 27 December 2025 (cottage cheese category value, age-cohort breakdown, Tesco growth); NIQ via The Grocer, April 2026 (Müller · Myprotein co-branded sales).

Corporate. Arla Foods 2025 Full-Year Results (February 2026); Lactalis Group Protein Works acquisition announcement (1 June 2026); Yoplait UK interview, FoodNavigator (August 2025).

Demographic and policy. Office for National Statistics, 2024-based National Population Projections; International Longevity Centre, Maximising the Longevity Dividend.

Clinical and scientific. British Dietetic Association sarcopenia practice resource; UK SACN Dietary Reference Values for protein; Frontiers in Nutrition, indicator amino acid oxidation study (March 2025); University College London / BMC Medicine GLP-1 prescribing analysis (2026); IQVIA UK dispensing data (July 2025).

More news and insight